The investment process should always begin by setting appropriate goals.

How can my adviser help me?

1. Your adviser can help you to set investment goals that are clear, measurable and attainable.

2. They can develop a plan based on these goals, taking into account your risk profile.

3. Finally, they can evaluate progress, usually either yearly or twice-yearly, helping you to stay on track or, if your goals or your circumstances change, suggesting appropriate adjustments.

The table below shows key elements that your plan might include:

| ITEM |

DEFINITION |

| Objective |

How much money you need to achieve a goal, such as retirement |

| Time horizon |

The number of years you have to the goal |

| Risk profile |

The level of risk you are willing to take to achieve your goals |

| Savings rate |

How much you can invest at the start, and regularly thereafter |

| Investment Mix |

The broad mix of investment types you’ll use to achieve your goal. Professional investors call this 'asset allocation' |

| Monitoring |

How your portfolio is going to be monitored and adjusted to keep it near its asset allocation target |

Why does it matter?

Investing without goals or a plan may simply lead to confusion. Should you ‘follow the money’ and invest in funds that are currently doing well? Should you maximise risk in the hope of getting the highest potential return? Different types of investment work in different ways. An investment in emerging markets will be very different to an investment in a UK government bond. You can only know which is right for you, or how to get the right balance between them, if you know what

you are trying to achieve.

It is unlikely that a single type of investment will provide everything an investor needs to achieve their long- term goals. A portfolio with a narrow range of investments is also likely to pose challenges for controlling risk. In most cases, for most investors, a well-balanced, diversified portfolio is likely to be the best solution.

How can my adviser help me?

1. Your adviser can help to choose the investments that are most likely to achieve your goals, while aimingto keep the portfolio’s short-term gains and losses within comfortable limits.

2. The portfolio is likely to comprise a diversified balance of shares and bonds. Shares tend to be higher risk, which is to say their valuations change constantly. Bonds, which are a form of loan, have pre-agreed repayment and interest rates. This means that their valuations tend to be steadier than shares, although they are also likely to have lower potential returns.

3. Investments in shares will help your capital to grow over the long term. Investments in bonds will help to sustain the overall value of your portfolio.

4. As the value of your different investments change, so will the proportion they take up in your portfolio. As part of the regular evaluation process, your adviser will help to maintain the portfolio at the right balance appropriate to your goals.

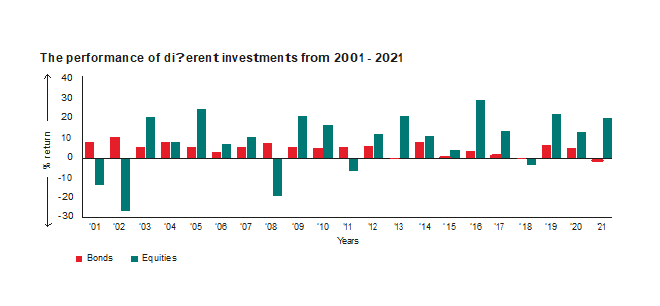

The graph below shows the risk/return trade-off between shares and bonds. While shares often have much bigger gains than bonds, they can also have much bigger losses.

Note* Always remember that past performance is not a reliable indicator of future results. The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future returns. The performance of an index is not the exact representation of any particular investment. As you cannot invest directly into an index, the performance shown in this table does not include the costs of investing in the relevant index. Basis of performance NAV to NAV with gross income reinvested 31 Dec 2001 - 31 Dec.

You can’t control the markets. You can’t control the economy. What you can control is how much you pay to invest. Fund costs vary widely and it can be surprisingly difficult to unpick the total cost of an investment, even more so for a diversified portfolio.

How can my adviser help me?

1. Speaking to your adviser about the impact of costs on long-term returns can be a key step towards investing success. That’s because the lower the charges, the more you get to keep of any return the funds achieve.

2. Your adviser should be able to identify the actual cost of investment, and can offer guidance on the funds most likely to give you the best value for money.

How can my adviser help me?

Every penny you pay in costs comes directly out of your return, reducing gains and worsening losses. Like interest, costs compound, but in reverse. Paying a pound in charges means you lose not just that pound but the returns it would have earned had it remained invested in your fund. Compounding, as we know, accelerates exponentially. Over time, the difference between a low- and a high-cost portfolio can have a major impact on returns.

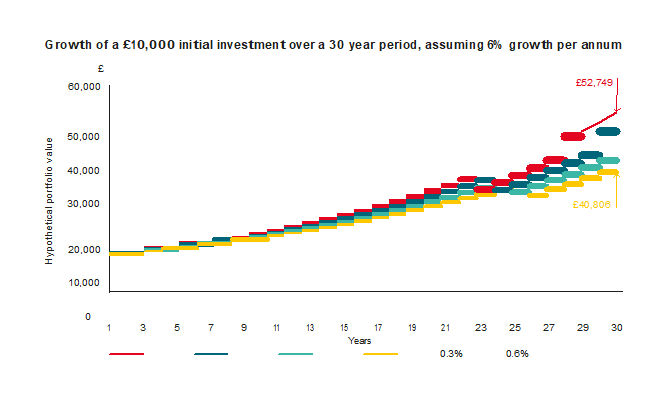

he hypothetical example below (which does not represent any particular investment) illustrates the potential impact of costs on an initial investment of £10,000 over a 30-year period. This graph assumes 6% average growth per annum which is compounded year on year. As this shows, fund expenses of 0.3% compared to 1.2% could potentially lead to savings of £11,943 over a 30-year period.

This hypothetical example assumes an investment of £10,000 over 30 years. Annual compounding is used for both the assump- tion of 6% average growth per annum and the investment costs. Costs are applied to average annual growth of 6% for each year. As it is hypothetical, this example does not represent any particular investment. Source: Todays Best Investments.

If you are investing to achieve a goal that is going to have a significant impact on your life, you are likely feel a wide range of emotions as the value of your portfolio rises and falls along the way. In our view – and there is data to show that this is true – investors that remain disciplined focusing on their long-term goals are more likely to succeed than those who chop and change in response to short-term conditions.

How can my adviser help me?

Our adviser can offer critical guidance to help you understand what is happening in the markets, and the importance of maintaining perspective and focusing on your goals.

Why does it matter?

There is a significant body of evidence that shows that, for most investors, most of the time, short-term or tactical positioning is unlikely to be better than staying the course. A portfolio that is not regularly rebalanced, which can mean selling rising assets and buying falling assets, is likely to become higher risk over time, which in turn will alter its potential returns.

It can often feel counter-intuitive to stay invested – or even to invest further – in investments that are falling in value, or to sell assets that are rising in value. An adviser can help you to understand the benefits of keeping your portfolio in balance, and why you should avoid the potentially costly mistakes of chasing short-term gains.

The chart below illustrates portfolio rebalancing. This can be achieved using an all-in-one multi-asset fund solution or through:

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results.

Important information

Todays Best Investments only gives information on products and services and does not give investment advice based on individual circumstances. If you have any questions related to your investment decision or the suitability or appropriateness for you of the product[s] described in this document, please contact your financial adviser.

Nothing in this document is intended to, or shall be deemed to, establish or evidence any partnership or joint venture between Todays Best Investments Asset Management Limited or any other Todays Best Investments entity and the issuer of this document nor authorise the issuer of this document to make or enter into any commitments for or on behalf of any Todays Best Investments entity.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.